How $0 trading fees help UAE investors build wealth faster

Trading commissions look small on paper. A few dollars per trade, a fraction of a percent of the order value. Most investors barely register them. Over a decade of regular investing, though, those small charges quietly remove thousands of dollars from your final portfolio, and the loss compounds in exactly the same way your gains do.

This article looks at what no commission trading UAE platforms actually offer, what traditional brokers charge, and what the difference adds up to over ten years of consistent investing. The maths is less dramatic than a market crash and considerably more predictable. That predictability is precisely why it deserves your attention.

What zero trading fees actually mean

When a platform advertises zero trading fees UAE investors should understand what is, and is not, included.

A true $0 commission structure means you pay nothing to place a buy or sell order for stocks and ETFs. The full amount you invest goes into the asset. If you invest $500, you own $500 of the security, not $484 after charges.

What zero commissions do not eliminate:

Regulatory and exchange fees.

Tiny charges imposed by exchanges and regulators on certain transactions. These exist on every platform and are usually fractions of a cent per share.

Currency conversion.

If you fund your account in dirhams and buy US-listed stocks, a conversion happens somewhere. Some platforms charge an FX spread; others pass through close to the interbank rate. This cost is separate from commission and worth checking.

Withholding tax on dividends.

US-listed stocks pay dividends subject to a 30% US withholding tax for non-US investors. This applies regardless of which broker you use; it is a feature of US tax law, not a platform charge. UAE residents pay no additional local tax on those dividends or on capital gains.

Advisory or management fees

If you use a managed portfolio service rather than trading on your own. These are charged annually as a percentage of assets and sit in a different category from per-trade commissions.

So the honest framing is this: zero commission removes one specific cost, the per-trade charge, completely. It does not make investing free. It does make the largest recurring, avoidable cost disappear, and for regular investors that single change carries real weight.

What traditional broker fees in the UAE look like

To understand what you save, you need a baseline. Traditional broker fees UAE investors face come in several layers.

Per-trade commissions at bank-owned brokerages

The brokerage arms of major UAE banks typically charge a percentage of trade value with a minimum per order. Emirates NBD's published schedule for US exchanges shows a trading fee of around 0.23% with a minimum of roughly $15.75 per trade. ADCB Securities charges about 0.275% on DFM trades plus a flat AED 10 per order. Other banks operate similar structures.

The minimum is the part that hurts. On a $10,000 trade, 0.23% is $23, annoying but proportionate. On a $500 trade, the $15.75 minimum represents 3.15% of your money, gone before the investment has done anything. Buy and later sell, and you have surrendered over 6% of the position to commissions alone. The smaller and more frequent your investments, the worse the minimum treats you.

Custody fees

Many traditional brokers and private banks charge an annual custody fee, often 0.1% to 0.5% of holdings, simply for holding your assets.

International transfer charges

Funding an overseas brokerage account from a UAE bank typically involves SWIFT transfer fees of AED 50 to 150 per transfer, plus exchange rate margins.

Inactivity and account fees

Some brokers charge monthly platform fees or penalise accounts that trade infrequently, which is a strange incentive to give a long-term investor.

Stack these together and a UAE investor making monthly contributions through a traditional bank brokerage can easily lose 2% to 4% of every contribution to friction costs before market returns enter the picture.

Fee drag: the 10-year compounding maths

Brokerage fee impact is best understood through a worked example, because the damage is not the fee itself. The damage is what the fee would have earned if it had stayed invested.

This is called fee drag, and you can think of what follows as a simple fee drag calculator on paper. The assumptions: an investor contributes $1,000 every month for ten years, markets return 7% annually (a common long-term planning assumption), and returns compound monthly. The figures are hypothetical and exist purely to illustrate the mechanics; real returns vary and are never guaranteed.

Scenario one: zero commission

The full $1,000 is invested each month. After ten years of contributions and compounding, the portfolio reaches approximately $173,000.

Scenario two: a traditional bank brokerage

Each monthly purchase costs $15.75 in commission, so $984.25 goes into the market. After ten years: approximately $170,300.

The gap is roughly $2,700. The investor paid about $1,890 in commissions over the decade, but the portfolio difference is larger than the fees paid, because every dollar handed to the broker in year one missed nine years of compounding. That is fee drag in action: the cost grows after you pay it.

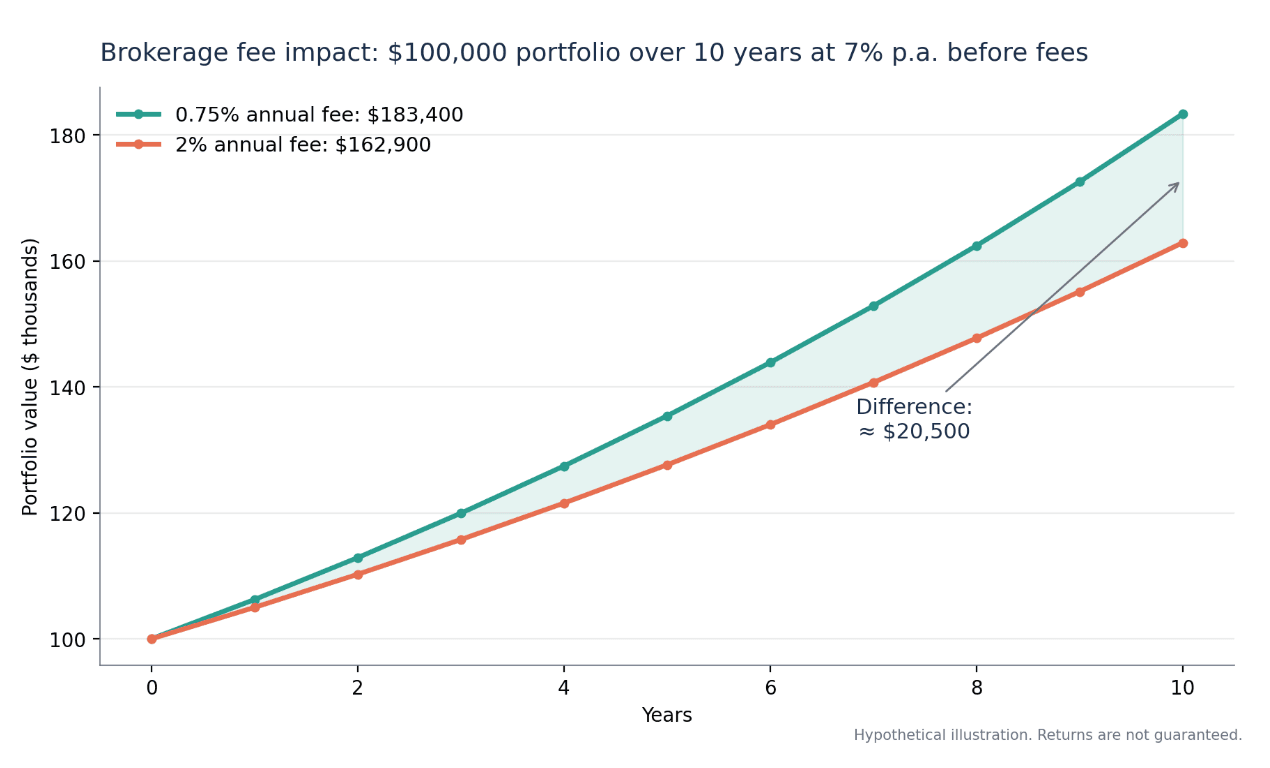

Now extend the logic to annual percentage fees, where the effect is stronger still. Take a $100,000 portfolio growing at 7% a year before fees, left alone for ten years:

At a 2% annual fee (typical of traditional discretionary management), the net return is 5% and the portfolio reaches about $163,000.

At a 0.75% annual fee, the net return is 6.25% and the portfolio reaches about $183,000.

Same market, same starting point, same decade. The difference is roughly $20,000, and it came entirely from costs. Nobody made a clever trade to earn it. Nobody took extra risk. The money simply was not given away.

This is the core insight behind 10-year compounding and zero trading fees UAE platforms now offer: investors spend enormous energy trying to add 1% to their returns through stock selection, which is hard, while a 1% cost reduction is available to anyone willing to compare fee schedules for an afternoon.

Cost comparison: UAE platforms side by side

The UAE retail investing market has become competitive, which works in your favour. Here is how the main categories compare on costs for self-directed stock and ETF trading. Fee structures change, so verify current figures on each provider's own pricing page before deciding.

Traditional bank brokerages

(Emirates NBD Securities, ADCB Securities, and similar): percentage commissions of roughly 0.15% to 0.3% per trade with substantial minimums, often $15 or more for international markets, plus custody and transfer charges in many cases. Strong for direct access to local exchanges (DFM, ADX) and for investors who want everything inside their existing bank relationship.

Sarwa

A well-established UAE digital platform regulated through ADGM, offering both a robo-advisory service and self-directed trading. According to Sarwa's pricing page, Sarwa Trade charges the greater of $1 or 0.25% of traded value per stock or ETF trade, with a $500 account minimum. Its managed portfolios carry tiered annual fees of roughly 0.40% to 0.85% depending on account size.

CUSP Wealth

A platform established by a firm regulated by the DFSA offering zero basic trading commissions on more than 10,000 US and US-listed international stocks and ETFs, with self-directed investing available from $1 through fractional shares. Managed (Personalised) Portfolios start from $25 and carry a 0.75% annual advisory fee. Assets are held with a US custodian under the investor's own name, with SIPC protection up to $500,000. SIPC protection applies in the event of broker failure and does not protect against investment losses.

Here is the Sarwa vs CUSP Wealth comparison at a glance

Figures reflect each provider's published information as of June 2026 and may change; check both platforms directly before deciding.

CUSP Wealth | Sarwa | |

Regulator | DFSA (DIFC), Category 4 retail licence | FSRA (ADGM) |

Stock & ETF commission | $0 trading fees* | Greater of $1 or 0.25% per trade |

Investable universe | 10,000+ US and US-listed international stocks and ETFs | 10,000+ US stocks and ETFs |

Minimum to start | $1 self-directed (fractional shares); $25 for Personalised Portfolios | $500 account minimum |

Managed portfolio fee | 0.75% per year | 0.40% to 0.85% per year, tiered by account size; minimum monthly fee applies on smaller accounts |

Fractional shares | Yes | Yes |

Shariah-compliant options | Yes; 1,300+ screened assets, platform is certified by Amanie Advisors | Yes; Halal portfolios available |

Custody and protection | Alpaca Securities LLC (US custodian), assets held in the investor's own name, SIPC protection up to $500,000. SIPC protection applies in the event of broker failure and does not protect against investment losses | Regulated third-party custodians; structure varies by product |

Other products | High-yield cash on uninvested funds | Options ($4 per contract), crypto (1.5% spread), savings |

Human advisor access | Yes, alongside AI-driven portfolio advice | Yes, including dedicated advisors on premium tiers |

On the narrow question of per-trade cost, the Sarwa vs CUSP Wealth comparison is straightforward arithmetic. An investor making one $1,000 trade per month pays $30 a year at $2.50 per trade (0.25% of $1,000), and $0 on a zero commission structure. Modest. But an investor making smaller, more frequent trades feels the difference more: ten $200 trades a month at the $1 minimum each is $120 a year versus zero. Over a decade, with compounding, those differences follow the fee drag mathematics above.

Both platforms are established by companies regulated by a financial regulator, both are far cheaper than the traditional alternatives, and both publish their fees openly, which already puts them ahead of much of the market. The right choice depends on which features you value beyond price: account minimums, portfolio options, Shariah screening, advisory access, and how each platform handles currency conversion. Personalised Portfolios start from $25 and carry a 0.75% annual advisory fee.

How zero fees change investor behaviour

The most underrated effect of no commission trading UAE platforms is not the money saved directly. It is the behaviour the pricing structure makes possible.

Small, regular investing becomes rational

Under a $15 minimum commission, investing $200 a month is irrational; the fee consumes 7.5% of every contribution. Investors respond by saving up for larger, infrequent trades, which keeps money sitting in cash for months and invites attempts to time the entry. With zero commissions, investing every payday in any amount costs nothing extra. Dirham-cost averaging becomes practical at any income level. For wealth-building UAE professionals earlier in their careers, this lowers the starting line considerably.

Fractional shares make sense

Zero commission platforms typically support fractional investing, so $50 buys $50 of an index ETF regardless of the share price. Combined with no per-trade cost, this allows portfolios to be built and diversified with very small amounts. Start investing in the UAE with as little as $25.

Rebalancing carries no penalty

Keeping a portfolio at its target allocation requires periodic selling and buying. When every order costs money, investors postpone rebalancing to avoid fees, and the portfolio drifts away from its intended risk level. When orders are free, maintaining the right allocation costs nothing but a few minutes.

Diversification gets cheaper

Building a position across ten ETFs used to mean ten commissions. Now it means ten free orders. The cost barrier to proper diversification has simply gone.

There is a caution to attach here. Free trading removes a useful brake as well as a useless cost. Commission-free does not mean consequence-free, and platforms that make trading frictionless can tempt investors into overtrading, which damages returns through poor timing rather than fees. The investors who benefit most from zero commissions are long-term investing types who use the free structure to contribute regularly and rebalance occasionally, not to trade daily. The fee saving rewards discipline; it does not replace it.

Where zero fee platforms make their money

A reasonable question: if trades are free, how does the platform survive? Understanding the answer protects you from surprises.

The platform earns money in a few ways: advisory fees on managed portfolios (0.40%–0.85% per year), FX spreads when clients fund in dirhams and invest in dollars, interest on uninvested cash, premium subscription tiers, and fees on products like options.

This applies to the conventional platform only. The Shariah-compliant mode works differently, interest income isn't permissible under Islamic finance, so that revenue line doesn't apply there.

None of these is sinister, and a regulated platform must disclose them. What you are checking for is concentration: if a platform's only revenue is an aggressive FX spread, your "free" trading may cost more than a transparent commission would have. Read the full fee schedule, not the headline. A short list of questions covers it: what is the FX conversion rate and spread? Are there withdrawal fees? Is there an inactivity charge? What happens to uninvested cash?

DFSA and FSRA regulation helps here, since both regimes impose disclosure obligations. You can verify any platform's regulatory status on the DFSA public register before opening an account.

Choosing the best zero-fee broker in the UAE

Searching for the best zero-fee broker UAE residents can use will return plenty of listicles. A more reliable approach is to score platforms yourself against a short set of criteria.

Regulation first

DFSA or FSRA authorisation, verified on the regulator's register rather than the platform's homepage. This is non-negotiable; everything else is preference.

Total cost, not headline cost

Zero commission plus a wide FX spread can cost more than a small commission plus interbank-rate conversion. Model your own usage: how often you will trade, in what size, and in which currency, then calculate the annual cost on each platform's full schedule.

Custody arrangements

Confirm where assets are held and in whose name. Assets held with a regulated custodian under your own name, ring-fenced from the platform's balance sheet, with SIPC or equivalent protection, survive the failure of the platform itself.

Account minimums and fractional access

An entry point of a few dollars and fractional shares suit a monthly contributor very differently than a $500 minimum does. Match the structure to your saving pattern.

Product range

Self-directed trading, managed portfolios, Shariah-compliant screening, savings products: decide which you actually need. A platform that combines free trading with a managed portfolio option lets you run a disciplined core portfolio alongside a small self-directed allocation, all in one place.

Human access

Some investors never need to speak to anyone. Others want a qualified adviser available when markets fall 20% and the plan suddenly feels theoretical. Hybrid platforms offer that access without traditional pricing.

Common questions about zero commission trading in the UAE

Is zero commission trading really free?

The per-trade charge is genuinely zero on platforms that offer it, but investing always carries some costs: currency conversion when moving between dirhams and dollars, US withholding tax on dividends, and advisory fees if you choose a managed portfolio. The honest comparison is total annual cost across your actual usage, and on that measure zero commission platforms still come out far ahead of traditional brokerages for most retail investors.

Are zero-fee brokers safe to use in the UAE?

Safety depends on regulation and custody, not on pricing. A platform whose company is regulated by the DFSA or FSRA, holding client assets with a separate regulated custodian under the investor's own name, offers the same structural protections whether it charges commissions or not. Check the regulator's public register and the custody arrangements; ignore the fee structure when assessing safety.

Do zero trading fees apply to UAE local stocks?

Most zero commission platforms in the UAE focus on US-listed stocks and ETFs. Trading on local exchanges such as DFM and ADX generally still runs through bank brokerages or licensed local brokers, where percentage commissions and per-order fees apply. If local market access is important to you, factor those costs in separately.

The bottom line

Trading commissions are one of the very few variables in investing that you control completely. You cannot control market returns, interest rates, or inflation. You can control what you pay to participate, and the difference between a high-cost and a low-cost structure, compounded over a decade, is measured in thousands of dollars for an ordinary monthly investor and tens of thousands for a larger portfolio.

The UAE market now offers regulated entities’ platforms with zero trading fees, where the per-trade cost is gone entirely, minimums are negligible, and full fee schedules are published openly. For long-term investing, the strategy this enables is almost boring: contribute regularly, diversify broadly, rebalance occasionally, and let the decade do the work. Boring is what compounding likes best.

The fee you avoid today is money that stays invested, earning, for every remaining year of your plan. That is how $0 trading fees help UAE investors build wealth faster: not through any single dramatic saving, but through ten years of small losses that never happen.

Frequently Asked Questions

Is no commission trading in the UAE really free?

The per-trade charge is genuinely zero on platforms that offer it, but investing always carries some costs: currency conversion when moving between dirhams and dollars, US withholding tax on dividends, and advisory fees if you choose a managed portfolio. The honest comparison is total annual cost across your actual usage, and on that measure zero commission platforms still come out far ahead of traditional brokerages for most retail investors.

What is the best zero fee broker in the UAE?

There is no single answer, because the right platform depends on how you invest. The criteria that matter are regulation (DFSA or FSRA, verified on the regulator's register), total cost including FX spreads rather than headline commission, custody arrangements, account minimums, and whether you want self-directed trading, a managed portfolio, or both. CUSP Wealth and Sarwa are two regulated UAE options that publish their fees openly; compare them against your own trading pattern rather than relying on a generic ranking.

Are zero fee brokers safe to use in the UAE?

Safety depends on regulation and custody, not on pricing. A company regulated by the DFSA or FSRA, holding client assets with a separate regulated custodian under the investor's own name, offers the same structural protections whether it charges commissions or not. Check the regulator's public register and the custody arrangements; ignore the fee structure when assessing safety.

How much do trading fees cost over the long term?

More than the fee itself, because of fee drag. An investor contributing $1,000 a month for ten years and paying a $15.75 minimum per trade ends up roughly $2,700 worse off than one paying nothing, even though the commissions themselves total about $1,890. The gap is larger than the fees paid because every dollar handed to a broker early on misses years of compounding. On percentage-based annual fees the effect is bigger still: a 2% fee versus a 0.75% fee on a $100,000 portfolio costs around $20,000 over a decade.

Do zero trading fees apply to UAE local stocks?

Most zero commission platforms in the UAE focus on US-listed stocks and ETFs. Trading on local exchanges such as DFM and ADX generally still runs through bank brokerages or licensed local brokers, where percentage commissions and per-order fees apply. If local market access is important to you, factor those costs in separately.

How do commission-free platforms make money?

Revenue doesn't come from per-trade charges. It comes from advisory fees on managed portfolios, currency conversion spreads, interest on uninvested cash, premium subscription tiers, and fees on complex products like options. Regulated platforms have to publish their full fee schedules, so none of this should be buried. What's worth checking is concentration: a platform whose main income is an aggressive FX spread may end up costing you more than a transparent commission would.

This applies to the conventional platform only. The Shariah-compliant mode works differently, interest on uninvested cash isn't permissible under Islamic finance, so that revenue line doesn't apply there.

Are there Shariah-compliant zero-fee platforms in the UAE?

Yes. Several regulated digital platforms offer Shariah-compliant portfolios screened against Islamic finance principles, alongside their zero or low-fee trading. The screening standard varies between providers, so check who certifies the portfolios and how often holdings are reviewed. CUSP Wealth's platform, for example, is certified by Amanie Advisors' Shariah Supervisory Board.

This article is for informational purposes only and does not constitute financial advice or a solicitation to invest. All figures are illustrative, based on hypothetical assumptions, and do not represent actual or projected returns of any product. Third-party fee information is drawn from publicly available sources as of June 2026 and may change; please verify current fees directly with each provider. Zero basic trading fees apply to specific assets as set out in CUSP Wealth's fee schedule. Cusp Wealth Ltd is regulated by the DFSA with a Category 4 license and DFSA’s Islamic endorsement to serve Retail Clients under license number 10863 and reference number F011420. All investments involve risk, including the possible loss of principal. Past performance is not a reliable indicator of future results. You should seek independent financial advice from a suitably qualified adviser before making investment decisions.